The International Air Transport Association (IATA) has released its methodology for accounting and reporting the emissions reduction associated with the use of Sustainable Aviation Fuel (SAF) by airlines.

SAF is an essential component of airline plans to achieve Net Zero carbon emissions by 2050.

The methodology, developed in collaboration with 40 airline experts globally, comes ahead of the IATA SAF Registry which is is expected to play a key role in creating a functioning global SAF market when it’s launched in April. It is feedstock-agnostic and technology-neutral.

In data entries, airlines should enter the neat SAF purchased in mass (kg or tonnes), volume in litres (cbm) or US gallons. If the neat SAF is not clearly stated, the blending ratio should be expressed.

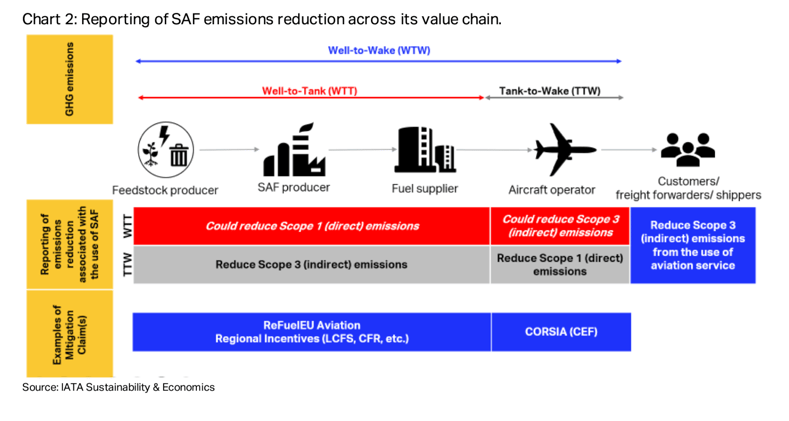

Emissions factor must be determined under Tank-To-Wake (TTW) or Well-To-Tank (WTT), through units of kg CO2/kg fuel kg or tonnes CO2/tonnes fuel.

Marie Owens Thomsen, IATA’s SVP Sustainability and Chief Economist, said its methodology will provide a consistent approach to accounting for the environmental benefits of SAF purchases, regardless of location.

“This is an essential component of the soon-to-be launched IATA SAF Registry which will enable airlines to claim SAF benefits against their regulatory and voluntary obligations, irrespective of where SAF was uplifted. The transparency of a published global standard methodology will give confidence that the Registry is robust and fair, with no double-counting. This is essential in creating a functioning global SAF market,” she said.

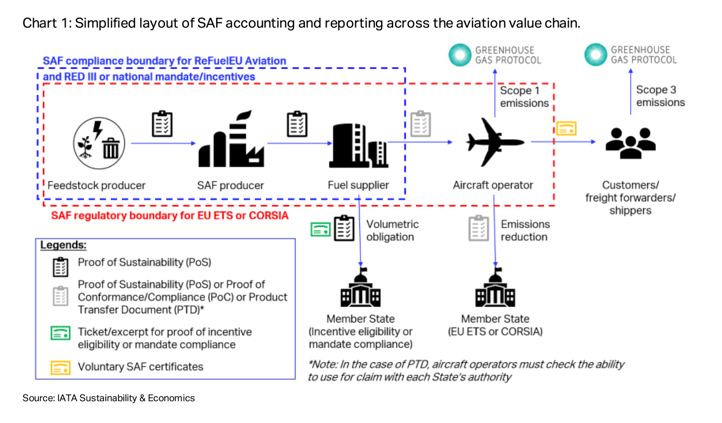

Removing double counting – where an airline or entity could claim the same emissions reduction benefits from a batch of SAF across multiple regulatory frameworks or voluntary schemes without proper accounting – is one thorny area.

It is recommended that airlines obtain a declaration from the fuel supplier that the SAF and associated benefits ‘belongs to the purchasing airline and have not been purchased or claimed by another party in the same emissions scope’.

Key features

- Purchase-based emissions calculations, irrespective of chain-of-custody used and SAF uplift locations, aligning with ICAO’s CORSIA approach

- Optional TTW) or WTW emissions factors to meet varying regulatory and voluntary requirements

- A consistent accounting approach to address regulatory and voluntary compliance needs

- No pre-judgement of additionality decisions by the claiming party, as long as no double counting occurs in the accounting of SAF emissions reduction

- Guidance for SAF emissions reduction in per-passenger and per-shipment calculations.

- Core principles

- A level playing field

- Prevention of double-counting

- Integrity in environmental and reporting claims

- Transparent, verifiable data

Under UK law, SAF must now make up at least 2% of all jet fuel in flights taking off from the UK this year, growing year-on-year to 10% by 2030 and 22% by 2040.

These targets should see around 1.2 million tonnes of SAF supplied to the UK airline industry each year by 2030, and deliver 6.3 megatonnes of carbon savings per year a decade later.

Capacity remains the main hurdle. In 2024, SAF production capacity didn’t exceed 1.5 million metric tonnes (Mt), barely 0.5% of total jet fuel needs, according to IATA estimates.

Read more: Is UK SAF mandate achievable?